What Financial Operational and Other Repercussions Is Your Hospital Now Subject to

Editor's Note: This white paper is part of the USC-Brookings Schaeffer Initiative for Health Policy, which is a partnership betwixt the Economic Studies Program at Brookings and the USC Schaeffer Center for Health Policy & Economic science. The Initiative aims to inform the national wellness care debate with rigorous, evidence-based analysis leading to applied recommendations using the collaborative strengths of USC and Brookings. This work was supported by a grant from the Robert Forest Johnson Foundation.

Under the Affordable Care Act (ACA), states accept the option to expand their Medicaid programs to all non-elderly people with incomes below 138% of the federal poverty level (FPL). To engagement, twelve states have not done then. In these states, people with incomes below 100% of FPL are mostly ineligible for any form of deeply subsidized coverage because subsidized Marketplace coverage is typically unavailable to people below the poverty line. Additionally, people with incomes between 100% and 138% of the FPL more often than not face higher price-sharing—and, until recently, faced college premiums—than in Medicaid.

The electric current draft of the Build Back Better Act (BBBA) proposes to fill this "coverage gap" by expanding eligibility for Market coverage to people beneath the poverty line in these states. It would besides make changes to Marketplace coverage for all people with incomes beneath 138% of the FPL to brand that coverage more "Medicaid-like," including eliminating almost all premiums and cost-sharing, adding coverage of certain services that are covered in Medicaid merely non typically covered in the Market place, and allowing people to enroll in subsidized coverage even if they are offered coverage at piece of work.

While the main beneficiaries of these changes would be low-income people in the coverage gap states, these coverage proposals would also have major implications for hospital finances.[1] This analysis uses the rich prove base produced by state Medicaid expansions to estimate these furnishings on hospitals.

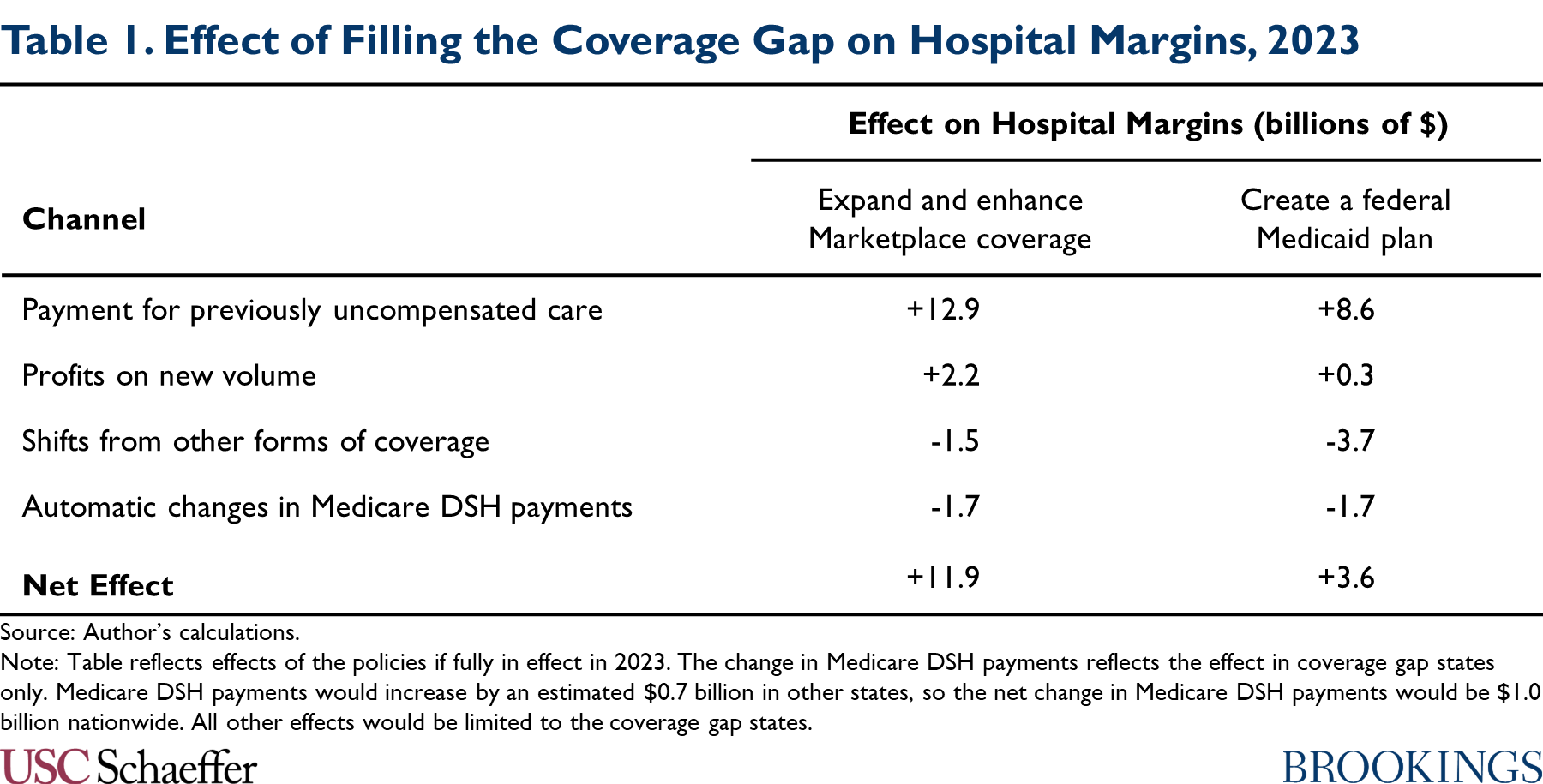

I estimate that amass infirmary margins in the coverage gap states would improve by $11.9 billion if the proposals in the draft BBBA were fully in event in 2023, as summarized in Tabular array 1. The main reason for this comeback is that hospitals would now receive payment for some intendance that they already deliver merely are not paid for; hospitals would also turn a profit from higher volume as people gaining coverage sought more than care. Those benefits would be partly offset by a minor migration of enrollees out of employer-sponsored plans, which probable pay hospitals more than Market plans. Hospitals in the coverage gap states would also receive smaller Medicare disproportionate share hospital (DSH) payments since those payments are set using a formula that takes into account the national uninsured rate and the allocation of uncompensated intendance across hospitals, both of which would change. (By contrast, I estimate that hospitals in expansion states would receive larger Medicare DSH payments.)

Hospitals in the coverage gap states would experience a smaller improvement in margins—$3.6 billion in my estimates—if policymakers instead filled the coverage gap by creating a federal Medicaid plan, as envisioned in an earlier Firm reconciliation proposal. A federal Medicaid plan would likely pay hospitals considerably less than Market plans. As a result, hospitals would receive less acquirement for previously uncompensated care, new book would be less lucrative, and shifts of enrollment from other forms of coverage into the federal Medicaid plan would cause a larger reduction in hospital revenues.

The typhoon BBBA would claw back a portion of the windfall to hospitals created past its coverage gap provisions, specifically by reducing Medicaid DSH payments and restricting Medicaid uncompensated care pools. An important question for policymakers as they finalize reconciliation legislation is whether to go further. Assuasive hospitals to retain part of this windfall could, in principle, benefit patients by allowing some hospitals, peculiarly less-resourced hospitals, to keep operating or invest in improving quality. On the other mitt, many hospitals might only accept higher profits or increase their costs in ways that do non meaningfully benefit patients, and recapturing these funds could give policymakers fiscal space to make improvements to the BBBA, such as continuing the legislation's coverage expansions later on 2025.

The remainder of this assay examines these issues in much greater item.

Two Approaches to Filling the Medicaid Coverage Gap

This analysis considers two unlike approaches to filling the Medicaid coverage gap: (1) expanding and enhancing subsidized Market place coverage, the approach taken in the draft BBBA; and (2) creating a federal Medicaid plan, the approach taken in an earlier House proposal. Equally described in particular below, either approach would offering a new subsidized coverage option to people in coverage gap states with incomes below the poverty line and make the coverage available to people with incomes between 100% and 138% of the FPL (who currently rely on the Market) more Medicaid-similar.[2]

Expand and Enhance Marketplace Coverage

The draft BBBA would fill the Medicaid coverage gap by extending eligibility for Marketplace subsidies (that is, the premium tax credit and price-sharing reductions available for Market plans) to people with incomes below the poverty line, who are generally non eligible for subsidized Market coverage at present. (Nothing would change for people in expansion states since being eligible for Medicaid would continue to make a person ineligible for subsidized Market coverage.)

The draft BBBA would also implement a diversity of changes to make Marketplace coverage more "Medicaid-similar" for all people with incomes beneath 138% of the FPL. In detail, changes to the premium tax credit would ensure that anyone in this group can enroll in the benchmark silver programme without paying a premium, mirroring the fact that Medicaid typically does not accuse premiums.[iii] These enrollees would also be eligible for a new, more generous tier of cost-sharing reduction that would offer an actuarial value of 99%, mirroring the nominal toll-sharing allowed in Medicaid, and require plans to cover services like non-emergency medical transportation that are mandatory in Medicaid simply non in the Marketplace. They would also exist exempt from the premium tax credit "reconciliation" process, which requires people who earn more than during a twelvemonth than they expect when they enroll to pay back office of their revenue enhancement credit.

The typhoon nib would too brand a variety of changes to the Marketplace enrollment process for these enrollees that would bring this coverage into closer alignment with Medicaid. These enrollees would not exist subject area to the "firewall" that bars most people offered employer coverage from obtaining subsidized Market coverage. They would also be permitted to enroll in Market coverage at whatsoever time during the year, rather than solely during the annual open enrollment period.[iv]

Since the coverage made available under these policies would exist like to Medicaid coverage in most salient respects, I presume that this suite of policies would affect insurance coverage and hospital volume (though not the prices hospitals are paid, as discussed below) in a manner similar to existing Medicaid expansions. This assumption allows me to draw on empirical evidence on the effects of existing expansions to estimate how this suite of policies would bear upon these outcomes.

However, there are plausible arguments for why the effects of these policies could differ from the effects of existing expansions.[five] Notably, the draft BBBA does not provide for "retroactive" coverage of services delivered during a menses prior to enrollment, coverage that is typically available in Medicaid. Additionally, considering the enrollment process would be administered past the federal government via HealthCare.gov, the provisions in the draft beak would not benefit from any integration with country social service agencies that may exist under Medicaid expansion. On the other hand, nether these policies, people in the coverage gap states with incomes above and below 138% of the FPL would be eligible for the aforementioned course of subsidized coverage, unlike under Medicaid expansion. This could increment insurance coverage relative to Medicaid expansion by reducing the risk that people who feel income volatility that causes their incomes to rise above or fall below this eligibility threshold experience a loss of coverage.[6]

The coverage gap provisions in the draft would phase in starting in 2022 and continue through 2025.

Create a Federal Medicaid Plan

Earlier typhoon reconciliation legislation released in September by the Firm Energy and Commerce Committee took an culling arroyo to filling the coverage gap (for years 2025 and later). That typhoon legislation would accept created a Medicaid-like federal program open to people living in Medicaid not-expansion states who would be eligible for Medicaid if their state adopted expansion.

The House typhoon envisioned that the coverage offered under this "federal Medicaid plan" would closely resemble Medicaid in about all respects, including benefit design, enrollment rules, and provider payment rates. As such, I assume that this policy would also affect insurance coverage and infirmary utilization in a way similar to existing Medicaid expansions, which again allows me to describe on the evidence base on the effects of Medicaid expansion in estimating the effects of this policy.

As above, there are arguments for why the effect of introducing a federal Medicaid plan could be larger or smaller than the effect of existing expansions. Like a Market place-based coverage gap program, a federal Medicaid plan would not do good from any integration with land social service programs that may be under expansion. On the other hand, because a federal Medicaid plan would exist federally administered, it might reduce the hazard of coverage loss amid people who experience a change in plan eligibility when their incomes rise higher up or fall below 138% of the FPL (although, dissimilar a Marketplace-based coverage programme, it would not eliminate these transitions entirely).

Policy Baseline

I guess the effect of each policy option relative to a electric current constabulary baseline. Notably, that means that the baseline for this analysis does non include an extension of the temporary expansion of the premium revenue enhancement credit included in the American Rescue Plan (ARP) Act. The effect of the coverage gap policies would likely be modestly smaller if analyzed relative to a baseline in which the ARP revenue enhancement credit enhancements were extended since those enhancements reduced the premium for the benchmark plan for people with incomes betwixt 100% and 138% of the FPL from merely over 2% of income to cypher, thereby closing some of the gap between Market place coverage and Medicaid coverage for this group.[7]

I besides presume that, under current police force, no states would prefer (or terminate) expansion through 2023, the year I focus on in my analysis. If states did begin or end expansion, the effect of policies filling the coverage gap would exist commensurately larger or smaller. Similarly, I assume that Wisconsin will continue to offer Medicaid coverage to people with incomes beneath the poverty line through its pre-ACA waiver program. Correspondingly, I simplify the assay by treating the policies considered hither equally having no effect in Wisconsin; in reality, they would have some result with respect to people with incomes betwixt 100% and 138% of the FPL, who currently receive Marketplace coverage in Wisconsin.

Estimating Financial Effects on Hospitals

Filling the Medicaid coverage gap would affect infirmary finances in several ways. Get-go, hospitals would now receive payment for some care that they already deliver but are not paid for. 2d, hospitals would profit from higher volume every bit the people who gained coverage sought more care. Tertiary, hospitals would lose revenue as some people switched into the coverage gap plan from individual plans that paid college prices. Fourth, some hospitals would lose Medicare DSH payments since payments under the program depend on the overall uninsured rate in the United States and the distribution of uncompensated care across hospitals, both of which would change. In what follows, I summarize how I estimate each of these furnishings and nowadays my results. The appendix provides boosted methodological particular.

Payment for Previously Uncompensated Care

Hospitals deliver a large corporeality of care for which they receive little or no payment. Much of this care is delivered in emergency situations since federal law requires hospitals to deliver emergency care without regard to the patient's ability to pay. Under a federal programme that filled the Medicaid coverage gap, some currently uncompensated care would become eligible for payment.

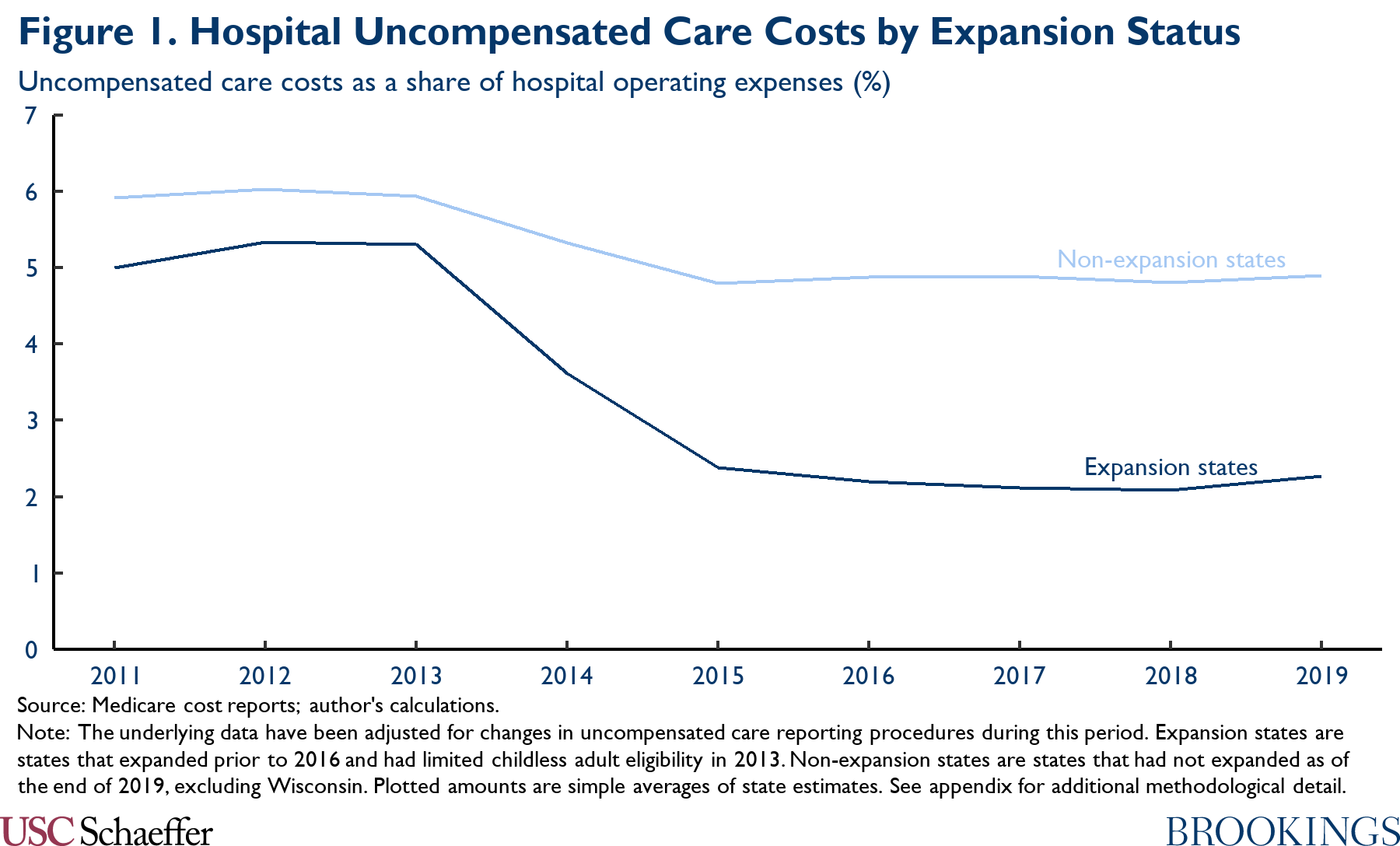

To quantify the resulting increase in hospital revenue, I examine trends in uncompensated care costs (as reported on hospitals' Medicare cost reports) later on implementation of Medicaid expansion in 2014, following a large prior literature that has estimated the outcome of Medicaid expansion on hospital uncompensated care. Figure ane replicates the basic finding that emerges from this literature: starting in 2014, the share of hospital expenses consumed by uncompensated care fell sharply in states that expanded Medicaid without declining similarly in states that did non expand Medicaid.

As described in the appendix, I use a difference-in-differences approach to distill the data underlying Figure 1 into state-specific estimates of the causal effect of Medicaid expansion on uncompensated care costs; my approach accounts for the possibility that Medicaid expansion (and the ACA'southward other coverage provisions) may have had different effects in states with dissimilar baseline characteristics. Using the results, I guess that the uncompensated care costs reported by hospitals in the coverage gap states would fall by $9.4 billion in 2023 if a coverage gap program were fully in consequence in that twelvemonth.

The ultimate effect on hospitals' bottom lines would depend on the prices the coverage gap program paid for the previously uncompensated intendance. I translate the estimated modify in reported uncompensated care costs into an estimated issue on hospitals' bottom lines by multiplying by the ratio of the coverage gap programme's infirmary prices to hospitals' boilerplate price of delivering intendance.[eight]

For the scenario where policymakers make full the coverage gap with a federal Medicaid program, I assume that the program would pay hospitals prices equivalent to Medicare's payment rates. Equally context, enquiry by the Medicaid and CHIP Access and Payment Commission (MACPAC) estimated that Medicaid payments to hospitals averaged 106% of Medicare's prices, simply this amount includes diverse forms of supplemental payments to hospitals that might not exist fully incorporated into payments fabricated by a Medicaid-like federal program.[nine] The Medicare Payment Advisory Commission (MedPAC) estimates that Medicare's prices currently cover 92% of hospitals' boilerplate costs, implying that the reduction in uncompensated care costs would ameliorate hospital margins by $eight.six billion in 2023 in this policy scenario.[ten]

For the scenario where policymakers fill the coverage gap past expanding Marketplace coverage, estimating the prices hospitals would receive is more challenging since there are no published estimates of the prices that private market plans pay for hospital care. As a general matter, information technology is ordinarily believed that these prices are higher the prices paid by Medicare and lower than the prices paid by employer-sponsored plans, with the latter belief ofttimes attributed to individual market place plans' narrower provider networks.[11]

Consistent with that view, inquiry by Lissenden and colleagues using information that individual market place insurers submit for gamble adjustment purposes finds that per enrollee claims spending was 29% lower in the private marketplace than in large employer plans in 2017, later adjusting for wellness status differences. A portion of that difference likely reflects differences in utilization rather than prices since narrow networks and other features of private market plans may reduce utilization relative to employer plans (in addition to reducing prices). On the other hand, to the extent that private market plans are able to negotiate lower prices than employer plans, it is plausible that those toll reductions are concentrated in the hospital sector since that is where concerns most provider marketplace power are most acute.

In the absenteeism of better information on this question, I therefore assume that the prices individual market plans pay hospitals are 29% lower than those paid by employer plans. Research by and large finds that employer plans pay around twice what Medicare pays for inpatient hospital care and somewhat more than than that for outpatient hospital care. Adopting the specific estimates of employer prices presented by Chernew, Hicks, and Shah and weighting inpatient and outpatient care as described in detail in the appendix, I therefore estimate that a Market place-based coverage gap program would pay hospitals 149% of what Medicare pays for hospital services, which would comprehend 137% of hospitals' average costs. This implies that the reduction in uncompensated intendance costs would total $12.9 billion in 2023 in this policy scenario.

Profits on New Volume

Research examining Medicaid expansion has generally plant that that people who gain health insurance under expansion use more care, and it is probable the same would be true under a program that filled the Medicaid coverage gap. If the coverage gap program paid hospitals more than than their (marginal) price of delivering that intendance, this increase in volume would translate into college infirmary profits.

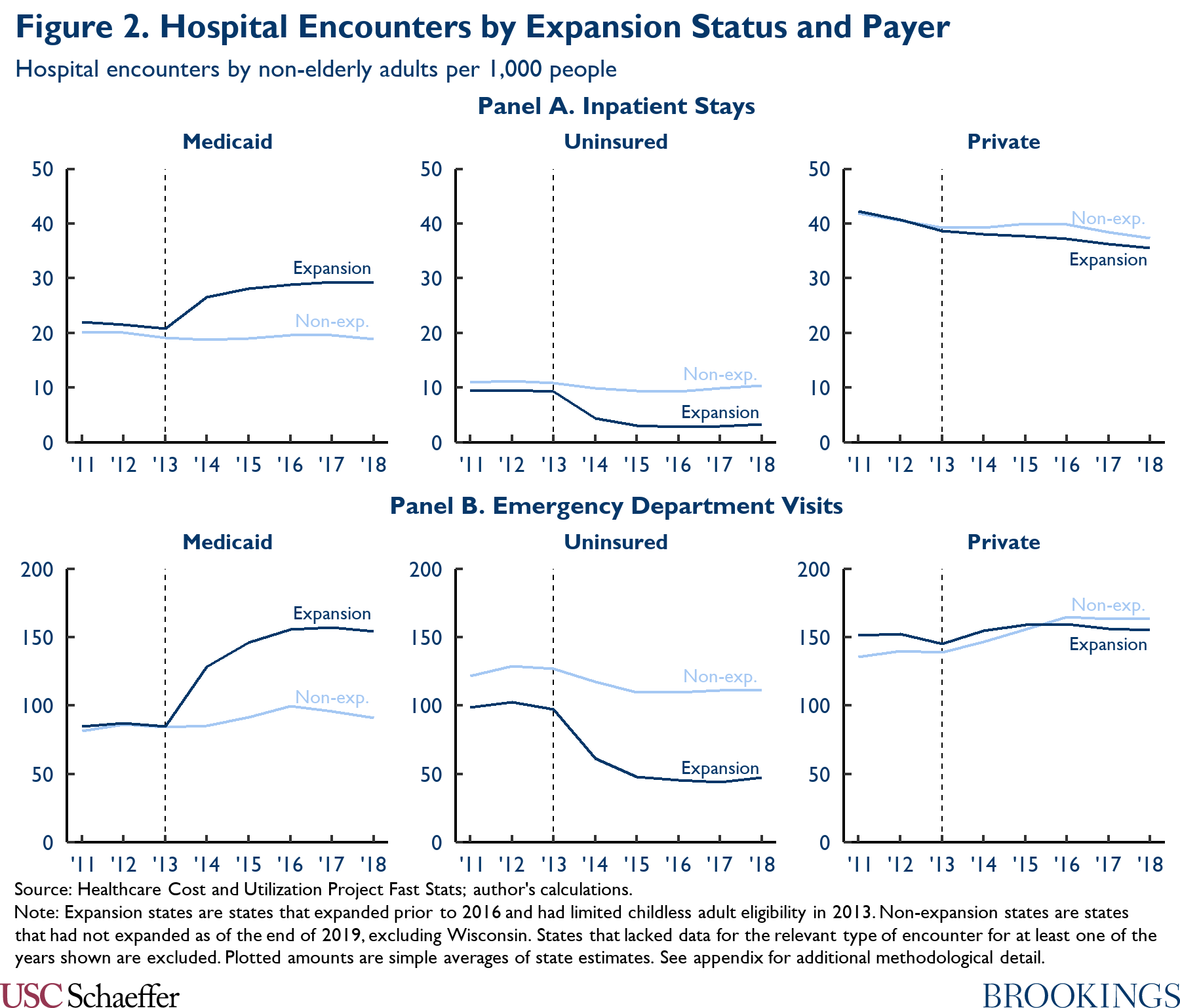

To gauge the effect on hospitals' bottom lines, I begin by examining how state Medicaid expansions have affected hospital utilization. To practise so, I use information from the Health Care Price and Utilization Projection, similar to the approach taken by Garthwaite and colleagues. Figure ii depicts trends in hospital utilization, disaggregated by payer and utilization type. Following expansion, Medicaid expansion states experienced a large (relative) increment in hospital encounters paid for by Medicaid. This gross increment in Medicaid encounters was offset in part, but seemingly non fully, by a substantial relative reduction in uninsured encounters and a smaller relative reduction in privately insured encounters.

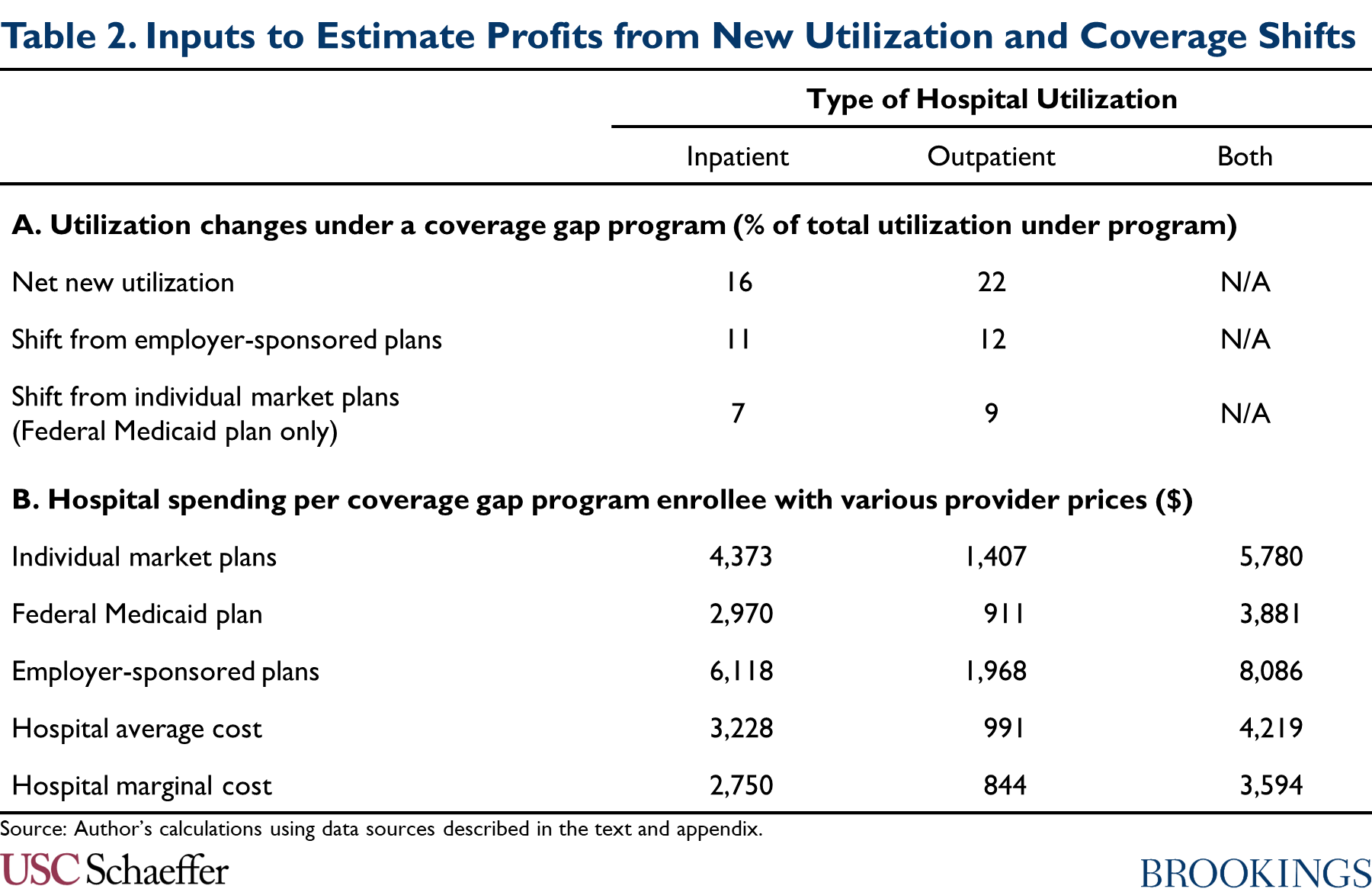

Once once again, I use a difference-in-differences approach to dribble the data underlying Figure 2 into land-specific estimates of the causal event of Medicaid expansion on infirmary utilization. Using those estimates, I estimate that xvi% of inpatient encounters and 22% of emergency section encounters paid for past a coverage gap program would represent cyberspace new utilization, as reported in Console A of Table 2.[12] (In the absence of information on all infirmary outpatient utilization, I use the estimate for emergency section encounters every bit a proxy for the respective estimate for hospital outpatient encounters overall.)

To obtain an estimate of the resulting issue on hospitals' finances, I multiply these shares past an gauge of the divergence between: (1) the aggregate amount a coverage gap program would pay for hospital intendance; and (2) the aggregate (marginal) costs hospitals would incur to deliver that care. I gauge those aggregate amounts by multiplying the acquirement hospitals would receive (and the costs they would incur) per person who enrolled in a coverage gap program past an estimate of total program enrollment.

I estimate per enrollee revenue using the post-obit data: CBO projections of benefit spending on Medicaid expansion enrollees; data from MACPAC, the Centers for Medicare and Medicaid Services, and Milliman on how spending is allocated across services; and the estimates of the prices paid by unlike payers described above. To estimate hospitals' marginal toll of delivering care, I use MedPAC's estimates that Medicare's prices were 8% in a higher place hospitals' marginal cost of delivering services as of 2019. The resulting per enrollee estimates are summarized in Panel B of Table two. Total details are in the appendix.

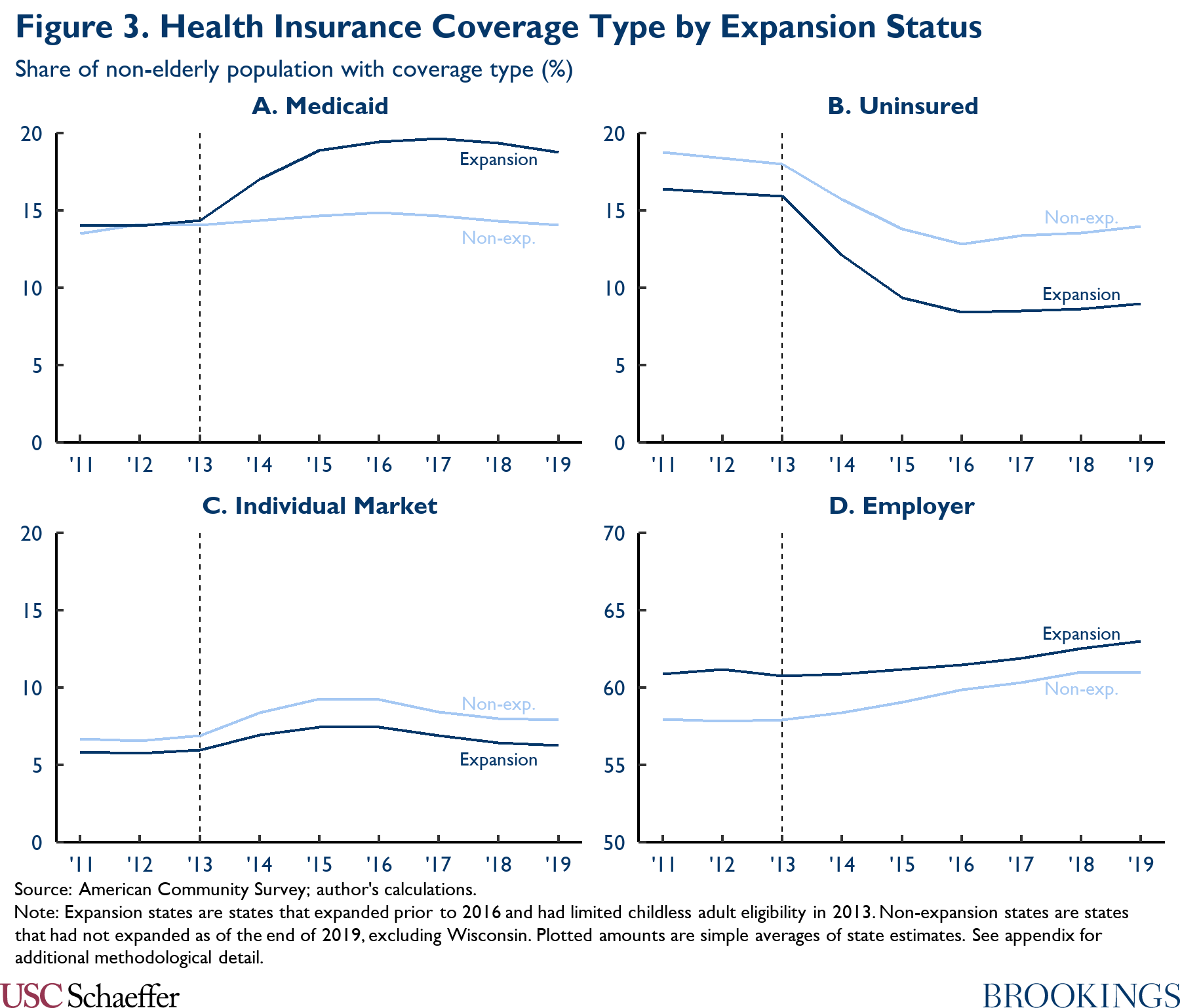

I judge enrollment in a coverage gap program by comparing trends in Medicaid enrollment between Medicaid expansion and not-expansion states, once again following substantial prior literature; these trends are depicted in Panel A of Figure iii. Every bit in other parts of this analysis, I use a departure-in-differences arroyo to convert the data underlying Effigy 3 into state-specific estimates of the causal effect of Medicaid expansion. Using these estimates, I estimate that 5.8 million people would enroll in a coverage gap programme, paralleling the big increase in Medicaid enrollment observed following expansion.

In this fashion, I estimate that hospitals' profits on new volume would corporeality to $0.3 billion nether a federal Medicaid plan and $2.2 billion nether a Marketplace-based coverage gap programme.

Transitions from Other Forms of Coverage to a Coverage Gap Program

A portion of the services paid for by a coverage gap program would likely be services that are currently paid for by individual insurance plans. That would occur for 2 chief reasons. First, some people who currently have employer-sponsored plans would probable opt for the coverage gap program instead because it offered lower premiums and out-of-pocket costs. Second, in the case of a federal Medicaid program, people with incomes between 100% and 138% of the FPL who are currently enrolled in subsidized Market place coverage would become eligible for the federal Medicaid plan instead. To the extent that a coverage gap program paid providers less than the plans enrollees shifted out of, hospital revenues would fall.[13]

To judge the event on hospital finances, I first estimate how much utilization would shift out of other forms of coverage. Equally above, I use a difference-in-differences approach to distill the data underlying Figure 2 into state-specific estimates of the causal effect of Medicaid expansion on hospital utilization by payer.[xiv] Applying those estimates to a coverage gap program, I gauge that shifts out of employer-sponsored coverage would account for 11% of inpatient utilization and 12% of emergency department utilization under a coverage gap program, as reported in Panel A of Table 2. Under a federal Medicaid plan, I judge that utilization that shifted out of private market plans would account for an additional 7% of inpatient utilization and 9% of emergency department utilization under the plan.

To obtain an guess of the effect on hospital finances, I multiply these shares by an estimate of the departure betwixt the aggregate corporeality a coverage gap program would pay for infirmary intendance and the aggregate amount that would be paid with alternative provider prices (either individual or employer market prices depending on the type of shifting involved). I calculate those aggregate estimates using the estimates of per enrollee infirmary spending in Panel B of Tabular array 2 and the guess of total enrollment in a coverage gap program reported in the last section. Using this approach, I estimate that hospitals would lose $1.5 billion through these types of coverage shifts under a Marketplace-based coverage gap program and a larger $3.7 billion through this channel from cosmos of a federal Medicaid plan.

Automatic Changes in Medicare DSH Payments

Medicare makes disproportionate share infirmary (DSH) payments to hospitals that are intended to outset hospitals' uncompensated intendance costs. Most of those payments are at present set using a formula established in the ACA.[xv] That formula establishes an aggregate national payment pool that scales up and downwards proportionally with the national uninsured rate and allocates the pool across hospitals in proportion to each infirmary's uncompensated care costs (as reflected on Medicare cost reports). Because filling the Medicaid coverage gap would reduce the national uninsured rate and uncompensated care costs in the coverage gap states, it would change the total amount and distribution of these DSH payments.

To estimate these effects, I begin by estimating the total amount of Medicare DSH payments that volition exist allocated based on uncompensated care costs under current constabulary; based on the pool established for fiscal yr 2022, I estimate this amount at $7.9 billion in agenda year 2023.[sixteen] Using the estimates of how filling the coverage gap would bear upon insurance coverage described to a higher place (and described further in the appendix), I estimate that a policy filling the coverage gap would reduce the national uninsured charge per unit by 12% if fully in event for 2023 and thus reduce this national pool of DSH payments by $1.0 billion.

To estimate how this modify would exist distributed across hospitals, I use the estimates of how filling the coverage gap would affect hospitals' uncompensated care costs that were described above to estimate aggregate uncompensated care costs in each state in 2023 under current police and under these policies. Under this approach, I estimate that hospitals in the coverage gap states would receive $i.vii billion less in Medicare DSH payments in 2023 if the coverage gap policies were fully in result than under current law. By contrast, hospitals in other states would receive $0.7 billion in boosted DSH payments. This occurs considering the reduction in uncompensated care in the coverage gap states would increase the share of uncompensated intendance accounted for past the expansion states, which would more than offset the reduction in the size of the national pool of uncompensated-care-based DSH payments.

I note that states as well make payments designed to beginning uncompensated care costs, including through the Medicaid DSH plan and through uncompensated care pools gear up nether Medicaid waivers. If implementation of a coverage gap program caused states to reduce those payments, that could too reduce hospital revenues. I exclude those reductions here considering implementing them would more often than not crave states to implement boosted policy changes. Additionally, states may be less likely to make these types of cutbacks if federal policymakers accept steps to claw back all or part of the benefits to hospitals from filling the coverage gap, so the estimates presented here may be a improve estimate of the full amount that federal policymakers could recapture from hospitals without leaving them worse off.

A Note on Culling Estimation Approaches

In this analysis, I gauge the effect of a coverage gap plan on hospital finances by explicitly specifying the channels through which a coverage gap program would affect hospitals and then estimating the effects that would ascend through each channel. An culling approach would be to direct estimate the issue that prior Medicaid expansions have had on hospital profit margins (presumably using difference-in-differences methods similar to those I use in the residuum of this analysis). This "direct" approach has some potential advantages relative to my "disaggregated" arroyo: information technology avoids the take a chance that I might fail to consider an of import channel through which a coverage gap program would bear on hospitals or that I might incorrectly guess the effects that would ascend through one of the channels that I do consider. Both of these risks are important sources of dubiety in the estimates I present hither.

Notwithstanding, the disaggregated approach I use hither has important advantages that, in my view, outweigh the potential advantages of the direct arroyo. First, my goal is to approximate how much infinite there is for policymakers to reduce other payments to hospitals without leaving hospitals worse off than they would be in the absenteeism of a coverage gap program. For that reason, my goal is to estimate the "daze" to hospital finances from filling the coverage gap—excluding any changes hospitals make to their operations in response to that daze. By dissimilarity, the direct approach estimates the realized alter in hospital margins acquired by Medicaid expansion, and, thus, incorporates the effect of whatsoever such operational changes. In particular, if positive fiscal shocks cause hospitals to increase their operating costs, so the realized alter in infirmary margins would underestimate the initial positive shock.

Second, the disaggregated approach I take hither makes information technology straightforward to account for ways in which a coverage gap program might differ from Medicaid expansion. In particular, it allows me to hands account for the fact that a Marketplace-based coverage gap program would likely pay prices well above Medicaid prices and, thus, accept a more positive event on hospitals' financial position than Medicaid expansion. Related, a disaggregated approach makes it clearer how effects on infirmary margins would ascend.

3rd, the evolution of hospital margins is influenced by many factors other than Medicaid expansion, notably including changes in the commercial pricing environment and changes in input costs. The effects of these factors are potentially big relative to the upshot of Medicaid expansion, which creates "groundwork noise" that reduces the precision of estimates obtained from the directly approach and opens the door to various forms of bias. By contrast, by building up the overall effect on hospital margins from estimates of the effect on outcomes where the influence of Medicaid expansion is larger in relation to the background noise, my disaggregated approach is less vulnerable (albeit non immune) to this concern.

Regardless, my estimates appear to be broadly uniform with prior inquiry that has used difference-in-differences methods to directly estimate how Medicaid expansion affected realized hospital margins. Notably, Moghtaderi and colleagues approximate that expansion improved the margins of expansion state hospitals by 0.5 percentage points, with a 95% confidence interval that extends from -0.five percentage points to ane.5 percentage points.[17] For comparing, I estimate that creation of a federal Medicaid plan would result in a $3.6 billion positive stupor to hospital margins if fully in consequence in 2023, which translates to ane.ane% of projected aggregate patient revenue in the coverage gap states in that yr.[eighteen]

Determination

This analysis estimates that filling the Medicaid coverage gap would meaningfully improve the finances of hospitals in the coverage gap states. I approximate that infirmary margins would amend by $11.9 billion relative to current law if the Marketplace-based coverage gap plan envisioned in the draft BBBA were fully in effect in 2023. The improvement in hospital margins would be smaller, but still substantial—$3.6 billion—if policymakers created a federal Medicaid plan, as envisioned in earlier House proposals.

An important question for policymakers as they work to finalize reconciliation legislation is whether they should effort to recapture all or role of these benefits to hospitals. Allowing hospitals to retain this windfall could, in principle, benefit patients past allowing some hospitals, especially less resourced hospitals, to go along operating or to make investments that improved quality of care. On the other hand, many hospitals might merely accept higher profits or increment their costs in ways that do not meaningfully do good patients, and recapturing some of the benefits to hospitals could give policymakers fiscal space to make improvements to the BBBA, such as continuing the legislation'southward coverage provisions past 2025.

The draft BBBA already contains some provisions aimed at clawing back some of the fiscal benefits to hospitals. Starting in fiscal yr 2023, the bill reduces Medicaid DSH allotments past 12.5% in not-expansion states; the resulting reduction in federal funding for Medicaid DSH payments would starting time at effectually $400 1000000 per twelvemonth and rise gradually over time.[19] The draft bill also imposes some limits on the scope of uncompensated care pools funded via Medicaid waivers non-expansion states. Estimating the bear upon of those provisions is beyond the scope of this analysis; however, the total amount of federal funding for existing uncompensated care pools is on track to total merely around $iv.4 billion per year, which provides an upper jump on the potential reduction in federal funding from this provision.[20],[21]

It thus seems clear that there is room to claw dorsum more coin from hospitals in the coverage gap states without leaving them worse off than they would exist without legislation filling the coverage gap. If policymakers wanted to go further in this direction, there are natural options for doing so. For example, they could implement larger reductions in Medicaid DSH payments in the coverage gap states or more tightly limit Medicaid uncompensated care pools. They could also consider reducing Medicare DSH payments in the coverage gap states. Even later the automatic reductions in Medicare DSH payments described above, I approximate that Medicare will still brand $iii.0 billion in uncompensated-care-based DSH payments to hospitals in the coverage gap states in 2023, with similar payments in subsequently years.

Footnotes:

[1] Throughout, I utilize the term "coverage gap states" to refer to the twelve non-expansion states other than Wisconsin. Wisconsin has non adopted Medicaid expansion, but offers Medicaid coverage to people with incomes beneath the poverty line through a pre-ACA waiver programme, and then coverage gap policies would have somewhat different—and generally smaller—effects in Wisconsin than in the other not-expansion states.

[two] Both proposals also include provisions designed to dissuade existing expansion states from ending their expansions. While a detailed assay of those provisions is beyond the telescopic of this piece, I exercise assume that these provisions would exist constructive, so neither policy would have directly effects in the current expansion states.

[3] For the purposes of this assay, I consider but the increase in the generosity of the premium tax credit that applies to people with incomes below 138% of the FPL, not the broader increases included in the draft BBBA.

[4] The administration recently made an administrative change that allows people eligible for zero-premium benchmark silver plans to enroll at any time during the yr. The provision in the draft BBBA provision would, in outcome, codify that policy with respect to the coverage gap population.

[five] At that place are also plausible arguments that the effect of Medicaid expansion could be smaller in the coverage gap states since those states might erect larger administrative barriers to enrollment. Considering federal coverage gap programs would non depend on state cooperation, this would not affect the applicability of bear witness from existing Medicaid expansions. However, this line of argument does suggest that a federal coverage gap program could take larger furnishings on the outcomes of involvement than Medicaid expansion in these states.

[6] Medicaid expansion itself could exist less effective in the coverage gap states than in other states since those states appear to be less motivated to expand coverage. This raises the possibility that experience with Medicaid expansion in other states could overstate the effect of Medicaid expansion in the coverage gap states and also that federal programs targeted at the coverage gap population (including both the draft BBBA proposals and a federal Medicaid plan) could have larger furnishings relative to Medicaid expansion in the coverage gap states.

[seven] While the comparison to a current law baseline is of involvement in its own right, one analytic advantage of focusing on this baseline is that the baseline policy environment closely resembles the one that existed when most existing information were collected and when most existing Medicaid expansions were implemented. This makes it more than straightforward to apply feel from the historical period to analyze the event of the coverage gap policies.

[8] This calculation would exist exactly correct if reported uncompensated care costs solely reflected the cost of delivering care to uninsured patients—and those patients fabricated no payment at all for that care. In reality, reported uncompensated care costs net out partial payments from uninsured patients and additionally include price-sharing obligations of insured patients that a hospital is unable to collect. The appendix considers this and related complications and concludes that these issues may engender a downward bias in my guess of the improvement in hospital finances, but that this bias is probable relatively slight, less than $ane billion under either course of coverage gap program. Thus, I retain the simplified calculation in the primary text for ease of exposition.

[nine] In particular, some of these payments are intended to defray a portion of hospitals' uncompensated care costs rather than compensate hospitals for treating Medicaid enrollees. Policymakers might non encounter the demand to expand the latter type of payments in the context of a program filling the Medicaid coverage gap.

[10] As a cantankerous-cheque on this estimate, I also estimated how much revenue hospitals would receive for care being delivered to people who are currently uninsured using the data on hospital volume past payer considered afterwards in this analysis. Under that approach, I estimated that hospitals would receive $fourteen.4 billion for this intendance nether a federal Medicaid plan and $21.4 billion under a Marketplace-based coverage gap program. Because those estimates do not net out any amounts hospitals are able to collect for care delivered to these uninsured patients (either from the patients themselves or from sources like indigent care programs), they are not directly comparable to the estimates that I derive based on reported uncompensated care costs. Taking account of that deviation, however, these estimates are broadly uniform with the uncompensated-care-based estimates.

[eleven] Features of the individual market other than differences in network latitude may also bear upon prices. Notably, enrollees may be more than sensitive to premium differences, which may in turn increase insurers' leverage when bargaining with providers, even holding a plan's network characteristics stock-still.

[12] Throughout, when I refer to services paid for past a coverage gap program or enrollment in such a program, I include people with incomes betwixt 100 and 138% of the FPL who already receive Market place subsidies.

[thirteen] Some patients might too transition from having their care paid for by country or local indigent care programs into a coverage gap program. Those transitions are not captured hither, but at least in the case of a Marketplace-based coverage gap program, they would likely generate some additional financial benefit to hospitals.

[14]The information underlying Figure 2 exercise non disaggregate utilization in individual market and employer-sponsored coverage. As described in the appendix, I utilise estimates of the effect of Medicaid expansion on each grade of coverage to split apart the overall modify in individual insurance utilization into its constituent components.

[fifteen] Medicare also makes some DSH payments using a pre-ACA formula based on how many Medicaid and Supplemental Security Income enrollees the infirmary treats. Payments nether the pre-ACA formula are also one of the inputs used to determine the national pool of uncompensated-intendance-based DSH payments. I assume that people enrolled in a federal Medicaid plan would not be considered Medicaid enrollees for Medicare DSH purposes, so neither policy considered here would affect Medicare DSH payments under the pre-ACA formula.

[16] The concluding rule setting Inpatient Prospective Payment System payment policies for federal fiscal twelvemonth 2022 establishes an aggregate uncompensated care DSH payment pool of $vii.2 billion. I trend that amount forward to fiscal years 2023 and 2024 using the March 2020 National Health Expenditure projections of Medicare hospital spending, and I then take a 25/75 weighted boilerplate of those amounts to become a calendar twelvemonth 2023 estimate.

[17] Other studies gauge larger (and statistically significant) positive effects on hospital margins. Equally Moghtaderi and colleagues note, however, the other studies in this literature take by and large weighted all hospitals equally, rather than assigning greater weight to larger hospitals. Since all of these studies agree that Medicaid expansion had larger positive furnishings on smaller hospitals, studies that apply equal weighting may overstate the positive effect on aggregate infirmary margins, which is what I aim to gauge hither.

[18] To estimate aggregate patient acquirement in these states in 2023, I begin with an guess of this amount as of 2019 derived from hospital price reports. I then trend this corporeality forward to 2023 using the National Health Expenditure projections of cumulative growth in aggregate hospital spending from 2019 to 2023.

[19] Full Medicaid DSH allotments for non-expansion states, as published by MACPAC, are $3.3 billion for fiscal twelvemonth 2022, of which 12.5% is $407 meg. Under current constabulary, aggregate national Medicaid DSH allotments will be reduced by $8 billion relative to the basic Medicaid DSH formula in fiscal years 2024-2027. But the language in the draft BBBA appears to be intended to calculate this additional reduction without regard to those reductions, and so this $407 million estimate is probable a reasonable guide to the outcome of the draft BBBA provision in futures years. In whatever example, the nationwide reductions have been repeatedly delayed past Congress and may never accept effect.

[20] These pools currently exist in Florida, Kansas, Tennessee, and Texas. I obtained information on the total size of each state's pool from the terms and conditions governing its waiver. For Florida, Kansas, and Tennessee, I used the approved amounts for the beginning year that extends into fiscal year 2023. For Texas, I used the amount currently in event since amounts for later years have not been determined. I determined federal funding for each state's pool by projecting forrard each state'southward federal share for fiscal year 2022, excluding the 6.two pct point increase in the federal share in effect under the Families Start Coronavirus Response Deed.

[21] In principle, the reduction in payments to hospitals under these arrangements could exceed the reduction in federal funding if states reduced their contributions to these programs. Even so, in the case of the uncompensated care pools in particular, the land's notional contribution to these programs is often ultimately provided past the hospitals themselves, so the telescopic for this to occur is express or not-existent.

Disclosures: The Brookings Institution is financed through the back up of a diverse assortment of foundations, corporations, governments, individuals, equally well equally an endowment. A list of donors tin be found in our annual reports published online here . The findings, interpretations, and conclusions in this report are solely those of its author(s) and are not influenced past any donation.

Acknowledgments: I thank Loren Adler and Richard Frank for helpful comments on a draft of this piece. I give thanks Kathleen Hannick and Conrad Milhaupt for excellent research assistance. All errors are my own.

Source: https://www.brookings.edu/essay/how-would-filling-the-medicaid-coverage-gap-affect-hospital-finances/

0 Response to "What Financial Operational and Other Repercussions Is Your Hospital Now Subject to"

Post a Comment